Tax Form 1099-B

1. 1099-B Summary of Proceeds, Gains & Losses, Adjustments and Withholding

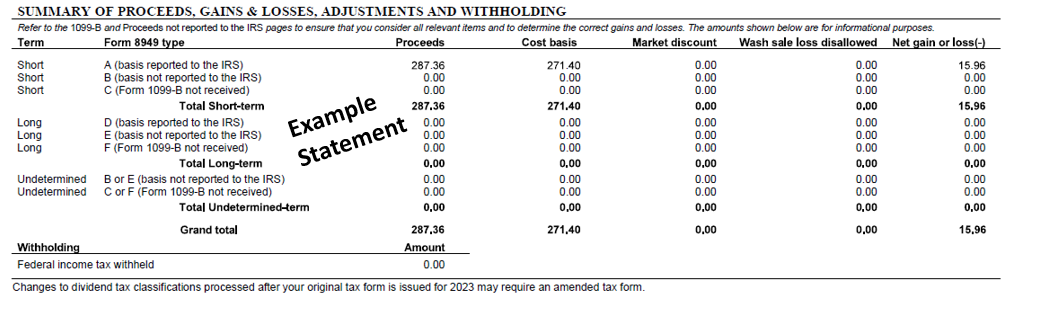

1.1 What is Form 1099-B (Summary of Proceeds, Gains & Losses, Adjustments and Withholding)

Form 1099-B (Summary of Proceeds, Gains & Losses, Adjustments and Withholding) is used to record customers' gains and losses from the sale of securities during a tax year.

1.2 Key Terms for 1099-B Summary of Proceeds, Gains & Losses, Adjustments and Withholding

1.2.1 Proceeds

The amount of money received from the sale of a security.

1.2.2 Cost Basis

The original/adjusted purchase price of a security. Cost basis is used to calculate capital gains or losses.

Average and Diluted Cost Basis are shown in the app but are not accepted by the IRS for 1099B reporting. Only the original/adjusted cost paid is reported.

○ The average cost of a stock (excluding commissions and fees) uses all the purchases (only) for a security to calculate the average. The diluted cost is the break-even price during the holding period, which means you can sell at this price without profit and loss (do not include commission and other fees). This method considers the profit and loss of every transaction (cash dividends and rights issues are not included) during the holding period. Both buy and sell executions change the diluted cost.

1.2.3 Market Discount

The discount received with the purchase of bonds.

Will be reflected as 0.00 as bonds are an unsupported product type.

1.2.4 Wash Sale Disallowed

Wash Sale- the sale of a security at a loss and a repurchase of the same security within 30 Days before or after the sale. With a wash sale, the loss is disallowed, meaning the loss cannot be used to reduce the amount of capital gains reported

1.2.5 Short term vs Long Term

Short term - securities were purchased and sold in 1 year or less.

Long term - securities were purchased and sold more than 1 year later.

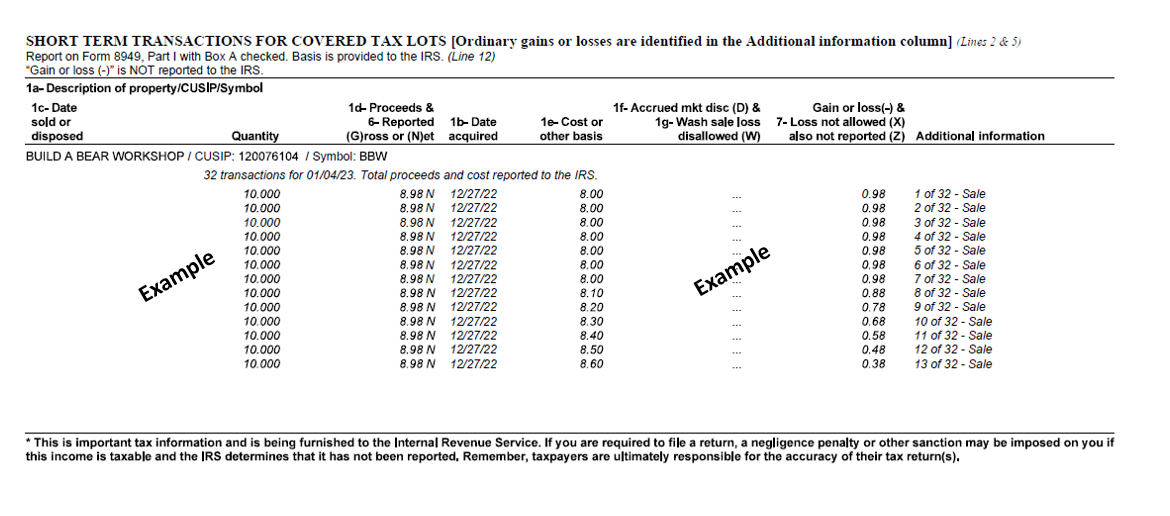

1.2.6 Covered vs Non-covered

Covered Securities report the cost basis, proceeds and gain/loss to the IRS for:

○ Stocks and ETFs purchased or acquired on or after January 1, 2011

○ Options acquired on or after January 1, 2014

Non-Covered Securities do not report cost basis or gain/loss to the IRS. Reporting of cost basis is the responsibility of the client.

1.2.7 Description of property/CUSIP/Symbol

Name and identifying information of security.

1.2.8 Date Sold or Disposed

The date of the sale.

1.2.9 Quantity

The number of shares sold.

1.2.10 Proceeds and Reported Gross/ Net

The amount of money received from the sale of security.

Gross amounts do not include any taxes or other deductions.

Net amounts include any taxes or other deductions.

1.2.11 Date Acquired

The purchase date of security.

1.2.12 Cost or other basis

The actual price paid to acquire security.

1.2.13 Accrued Market Discount

The discount received with the purchase of bonds (N/A).

1.2.14 Wash Sale Loss Disallowed

The loss of a sale that cannot be used to reduce the amount of capital gains reported.

1.2.15 Gain or Loss

The amount of profit or loss when a security is sold.

1.2.16 Additional Information

Details about the transaction or other useful information.

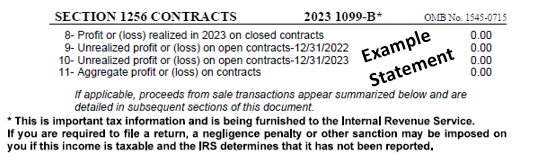

2. 1099-B Section 1256 Contracts

2.1 What is Section 1256 Contract

A Section 1256 contract is a type of investment defined by the Internal Revenue Code (IRC) as a regulated futures contract, foreign currency contract, non-equity option, dealer equity option, or dealer securities futures contract.

Section 1256 contracts are unique because each contract held by a taxpayer at the end of the tax year is treated as if it was sold for its fair market value, and gains or losses are treated as either short-term or long-term capital gains.

○ These contracts must be Marked to Market

■ Marked to market involves adjusting the value of an asset to reflect its value as determined by current market conditions. The market value is determined based on what a company would get for the asset if it was sold at that point in time.

○ These contracts will be reported using a 60/40 split:

■ 60% will be reported as an unrealized long term gain/loss

■ 40% will be reported as an unrealized short term gain/loss

Wash sales do not apply to Section 1256 contracts because they are marked-to-market.